Can you believe we’re almost halfway through the year? 2022 is right around the corner and before you know it Open Enrollment season will be here! To help us get prepared, we are taking time this week to discuss the recent IRS update for Health Savings Accounts and Dependent Care Assistance Programs.

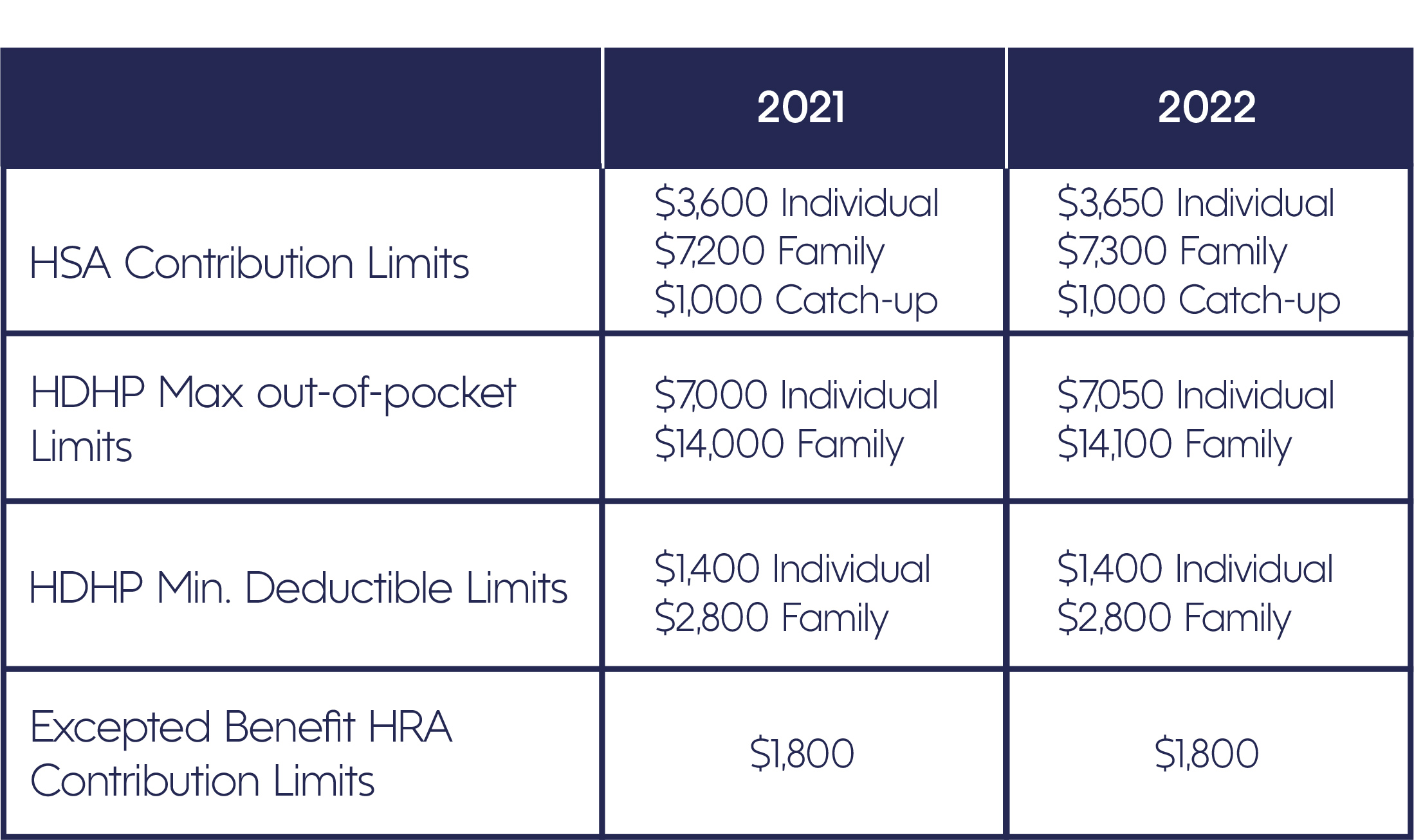

2022 HSA Limits

Last week the IRS issued Revenue Procedure 2021-25, providing the HSA cost-of-living contribution and coverage adjustments for 2022. It also includes the 2022 limit for Excepted Benefit HRAs. We broke it down in layman’s terms for you below, showing the changes from 2021 to 2022.

*Catch-up Limit applies to HSA holders that will be 55 or older by the end of this year. These participants can contribute an additional $1,000 to their HSAs, and this amount is per individual. All the contribution limits are adjusted for inflation annually except the catch-up contribution amount, which stays fixed.

*Excepted Benefits are types of coverage not included in a traditional health insurance plan, such as vision or disability coverage.

Dependent Care Benefits Update

Last week the IRS also released Notice 2021-26 providing guidance for 2021 and 2022 on the taxation of dependent care benefits under a Dependent Care Assistance Program (DCAP).

The Notice states that if the DCAP benefits were excluded from income during the tax year 2020 or 2021, the benefits can remain in exclusion from gross income, and are not wages for the employee in tax years 2021 and 2022. In addition, benefits will not be considered for purposes of the application of the limits under section 129 to other dependent care benefits available for 2021 and 2022.

Under section 129, amounts paid or incurred by the employer for dependent care assistance provided to the employee are excluded from the employee’s gross income. The income exclusion for 2021 is limited to $5,000 per tax year ($2,500 for a married spouse filing separately) or, if less, the employee’s (or employee’s spouse’s) earned income for the tax year. ARPA increased exclusions to $10,500 and $5,250, respectively, for 2021 only. Benefits remaining unused at the end of a plan year may, if the plan elects under Notice 2005-42, be used during an ensuing two-and-a-half-month grace period.

Please feel free to reach out to CDHP customer service with any questions about your account!